Market Commentary and You

Over the last 10 years the market has been in Bull territory with minor exceptions.

From 2012 to January of 2020 the consistency of the growth was unprecedented. January-March of 2020 brought a steep but short-lived decline due to the fear of the COVID-19 pandemic. The Dow Jones fell from 29,398 to 23,185…a 21% drop! However, this was one of the shortest Bear markets in our history. Within seven months the Dow had recovered all that it had lost. That short seven months was a fantastic buying opportunity for those that understand the market and are in their accumulation stage of retirement funding. Those that added to their positions in March of 2020 enjoyed investment returns in excess of 26% in just seven months! Of course, the market didn’t stop climbing in the fall of 2020. It would continue a climb to all-time highs of 36,799 at the end of 2021. The S&P 500 and NASDAQ enjoyed similar spectacular growth. Given the long duration (nearly 10 years), most investors had become accustomed to consistent and sustained growth with low volatility. Nearly every asset class produced gains, gains that were relatively smooth. During such periods “even a blind squirrel can find an acorn.” Then came January 2022.

After each of the market indices hit all-time highs around January 4th, significant volatility entered the markets. The indices have dropped more than 10% from their all-time highs just a few months ago. The technology sector has taken the hardest fall while energy has surged but on a bumpy path. Just in the last week we have seen 1,000-point swings from day to day.

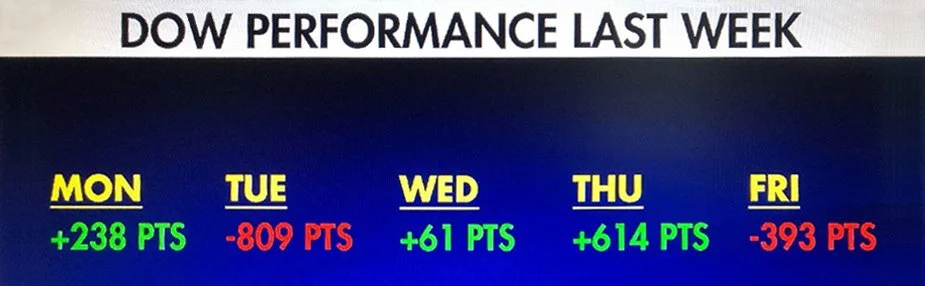

Above is an image illustrating the volatility of the DOW April 25th-29th.

On May 4th the DOW rose nearly 900 points. On May 5th the DOW lost 1,063 points. The selling continued into May 9th with the DOW losing another 653 points, and the NASDAQ taking it on the chin with a 521-point loss. While there are a number of economic factors contributing to this volatility (record inflation, energy costs, war in Ukraine, Federal Reserve interest rates, etc.), the focus of this newsletter is on fundamental investing and managing market volatility. You can’t time the market. Your individual risk tolerance and time horizon dictate how you should invest during turbulent markets.

Time Horizon: If you are nearing or in retirement you should invest very differently than if you are more than 10 years away from retirement. Why 10 years? The longest market decline going back to 1949 was 35 months (1959-1962) which dropped 14%. The steepest market decline was 52% (2007-09). The longest period to recover from a market decline was 8 years (1973-1980). These were the worst cases in the last 73 years and if combined would have covered 11 years. If you are more than 10 years from retirement then you are able to accept more risk with the purpose of growing your retirement nest egg.

Risk Tolerance: There are two aspects to risk tolerance. These are the financial capacity and the emotional capacity to absorb risk. The financial capacity is an income and volume issue. If you have a stable and/or substantial income that can offset declines or investment losses you have a higher financial capacity than someone that does not. However, it doesn’t matter how much wealth or your level of income if your emotional capacity for risk is low. Seeing the market go up and down can cause anxiety for those averse to risk. The inverse is also true. Someone may have a high emotional capacity for risk but lacks the financial resources to take on risk. Therefore, risk tolerance is a key component to asset selection and portfolio construction. A portfolio with the wrong risk tolerance for that investor will lead to the investor getting out of the market. The goal of a good investment advisor is to keep the client invested for the long-term with the most risk that is suitable for their circumstance. This will produce the best outcome for the investor over the long-term.

Near or in retirement: There are a number of factors that make every investor’s circumstance different, but generally those in this stage should have large positions in income generating investments (bonds, dividend funds/stocks, real estate, etc.). These assets classes tend to be less volatile while generating consistent yields. A great example for those in retirement is to have a position in I-bonds from the U.S. Treasury. They currently pay 9.62% and compound annually. The principal is guaranteed and the rate of return is adjusted for inflation. Not a bad choice for safe retirement income.

Accumulation Stage: This is the stage when an investor is accumulating retirement assets and contributing to retirement accounts. The asset selection is determined by risk tolerance and time horizon, but unlike being near or in retirement more risk is recommended. This would usually be in the form of growth funds/stocks that offer a higher potential for returns but are offset by increased risk and volatility. The “ups and downs” of higher risk assets can be absorbed because there is time to “recover” from the declines. The use of dollar-cost-averaging takes advantage of the “downs” by purchasing more at a discounted price. Keep buying as prices go down. Diversification is a fundamental that can “smooth out” a portfolio with proper asset selections and deliberate correlations. I also advocate for dividend reinvesting to “super charge” a portfolio by increasing the compounding of growth.

Through much of 2020 and 2021 the equity market was “overheated” and prices were over-valued. With the DOW down 11.26%, the S&P 500 down 15.85%, and the NASDAQ down 25.32% in 2022, valuations have become more reasonable and there are bargains to be had.

Tune out all the noise and maintain a wealth building and long-term perspective. Remember, “calm like panic is contagious.”

Sincerely,

Ty B. Kopke | Silver Oak Leaf Financial Services, LLC